Our Beliefs

We’re creating a new era in revenue cycle management driven by three core beliefs.

( 1 )

Comprehensive automation is the future.

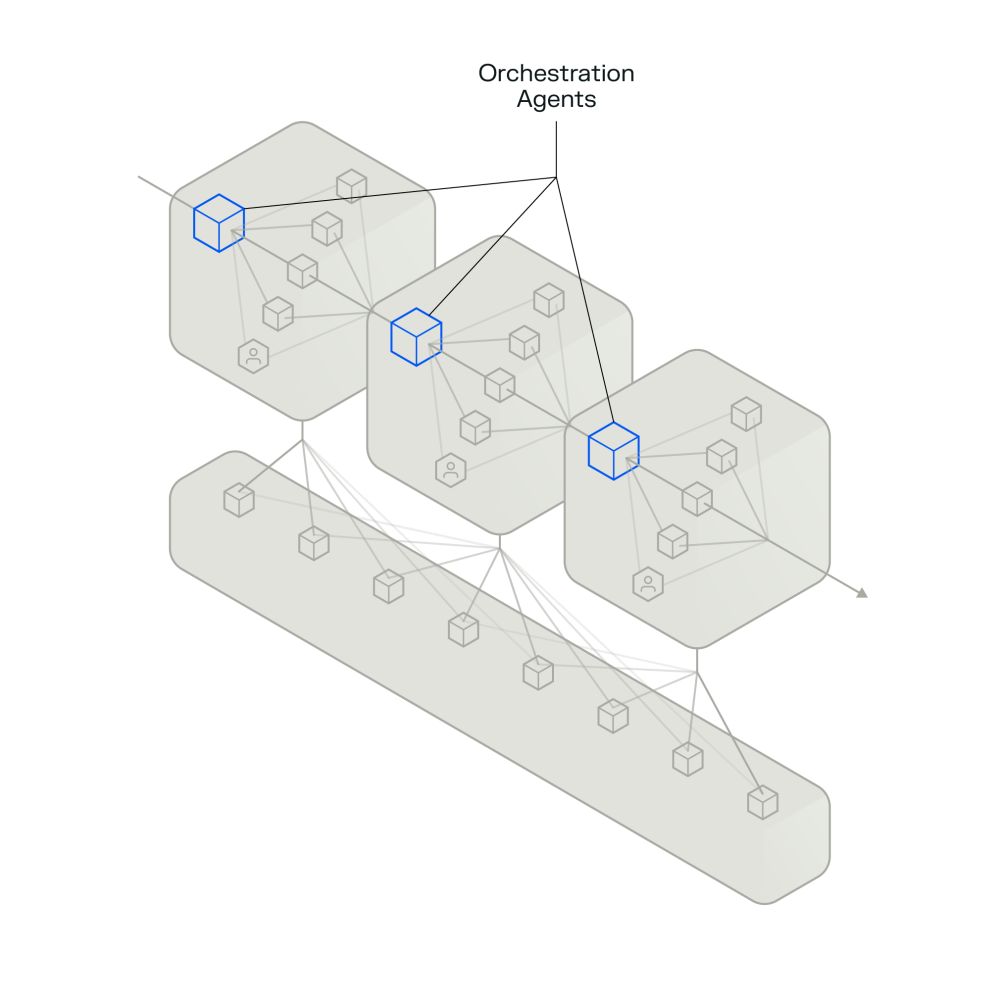

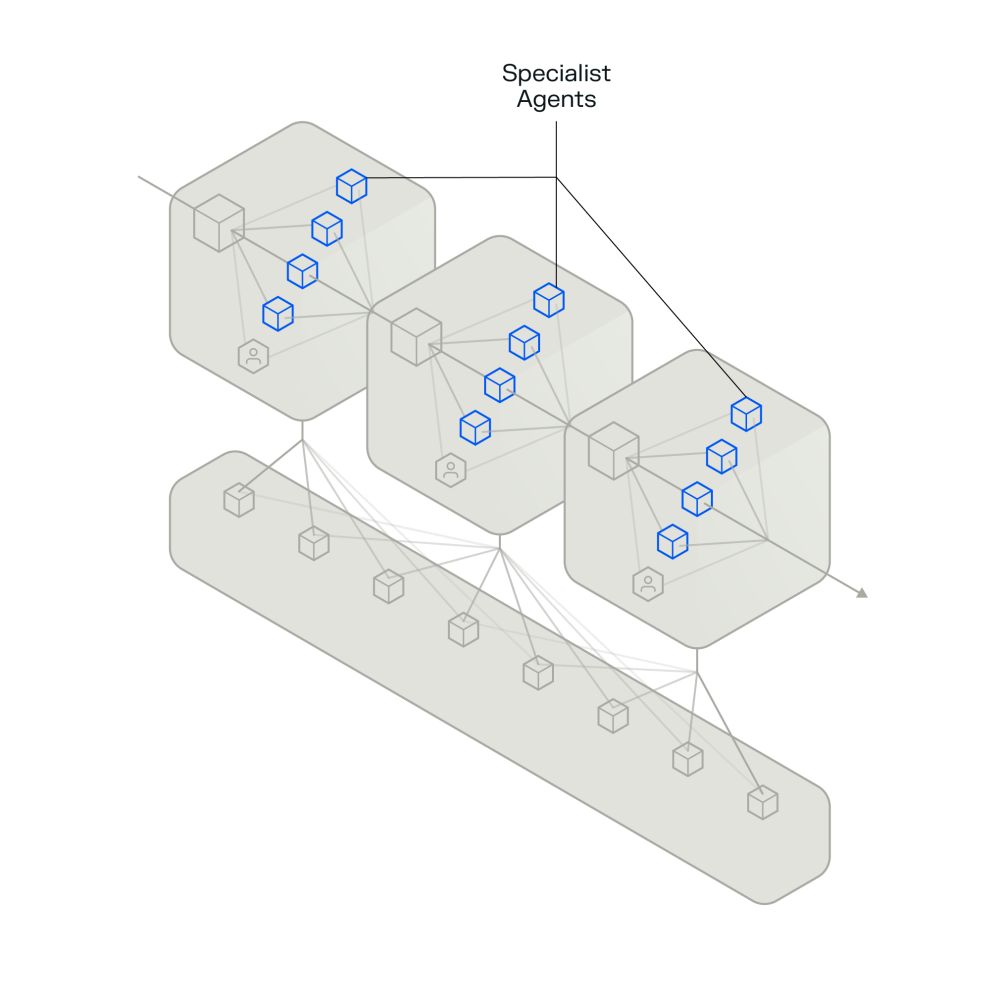

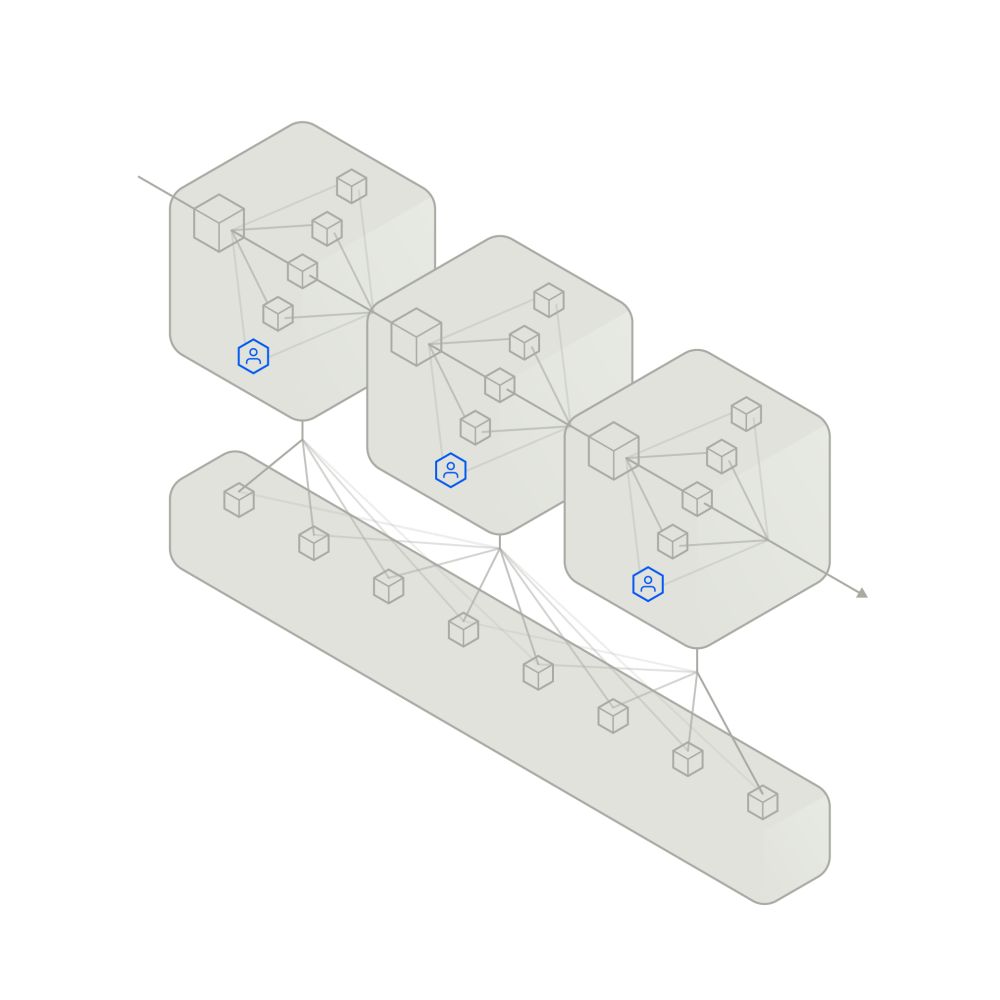

We believe in system level automation, powered by AI agents and orchestrated across the entire revenue cycle.

( 2 )

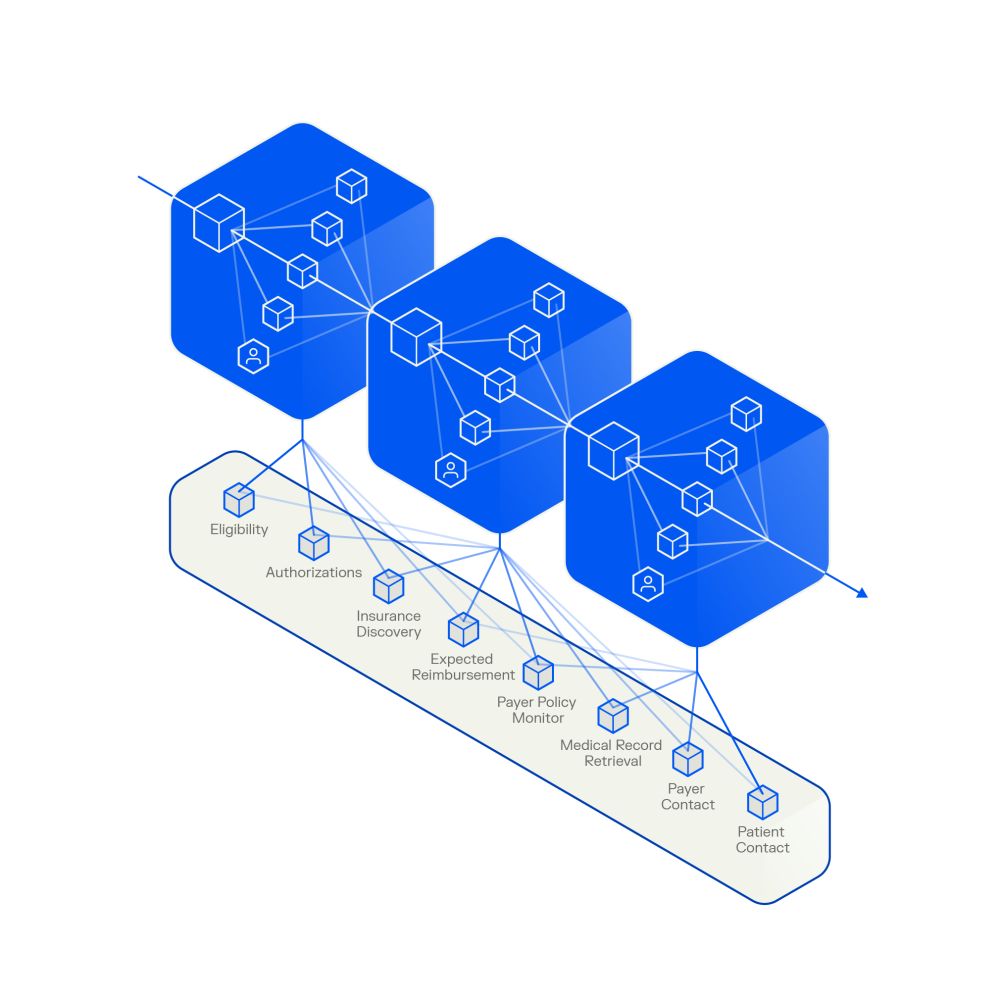

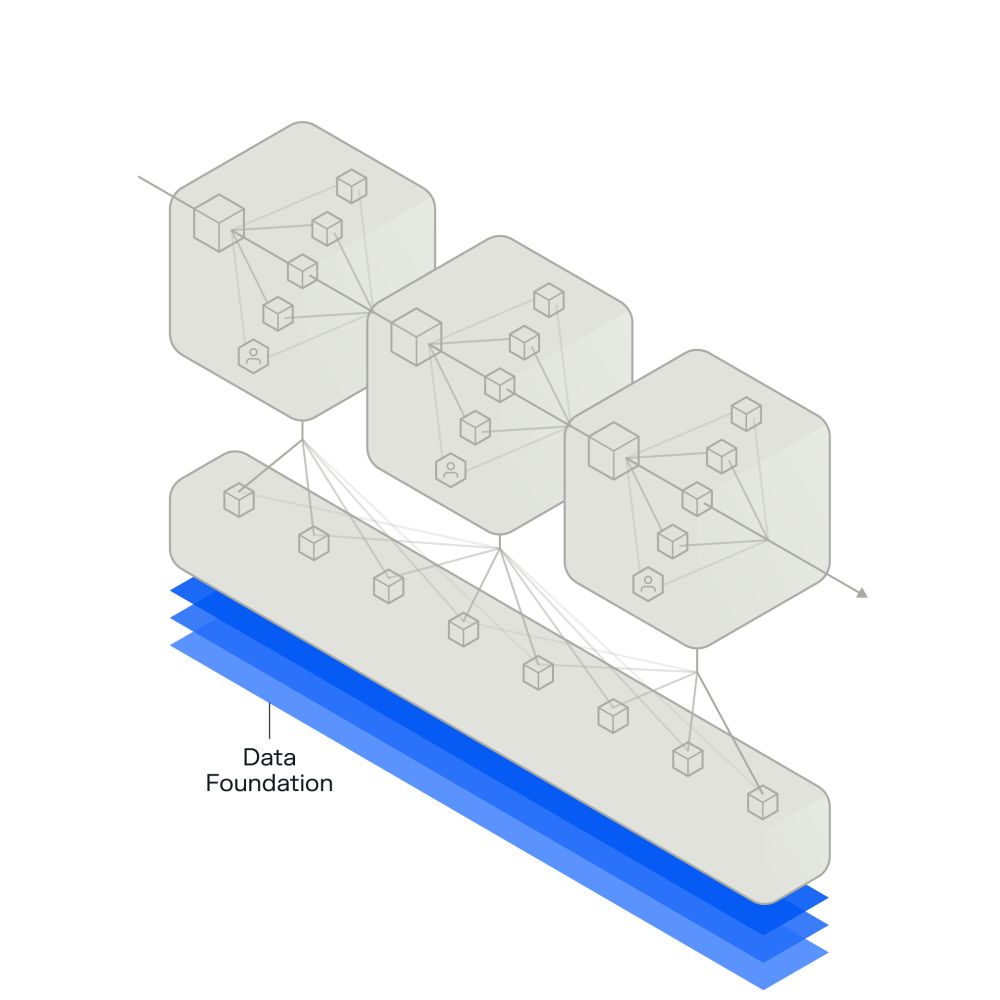

A system-level view is essential.

Effective automation requires a connected, contextual understanding of the full revenue cycle ecosystem.

( 3 )

Real-time adjudication is within reach.

AI makes it possible to align payer and provider incentives, resolve claims instantly and eliminate administrative drag.

Introducing

Phare: Healthcare’s First Revenue Operating System

-

Phare is a platform that automates complex work through an integrated agentic system.

Our Products

Our enterprise-grade AI products deliver transformational outcomes.

Phare Access

( 1 )

Phare Claim

( 2 )

Phare Flow

( 3 )

Our engagement models meet you where you are.

( 1 )

Operating partnerships

A longer term engagement where R1 manages revenue cycle operations and employees, leveraging our two decades of experience as operators and revenue cycle pioneers.

( 2 )

Agentic solutions

Expert R1 engineers partner with customers to integrate, implement and curate AI agents, maximizing performance over time.

R1's AI Lab

R37 is building technology that’s transforming the unit economics of healthcare.

An innovation engine

R37 is R1’s AI lab to transform healthcare financial performance. Our dedicated team of technologists and revenue cycle experts identify, build and scale AI solutions aimed at achieving comprehensive automation and moving the industry to real-time adjudication.

We utilize reasoning, language, voice and capture use models to build AI agents that are deployed as part of an integrated system. This system optimally allocates work between autonomous agents and humans. The results are increased revenue, reduced costs and faster throughput.